Welcome to WordPress. This is your first post. Edit or delete it, then start writing!

SBA 504 Program Overview

The SBA 504 loan program provides small businesses long-term, fixed-rate financing to acquire major fixed assets for expansion or modernization. Projects are secured by a 1st and 2nd Deed of Trust/Mortgage on General and Special Purpose commercial real estate, meeting SBA qualifications, having a maximum aggregate Loan to Value between of 90%, depending on program parameters.

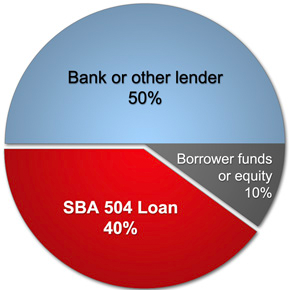

Typical project structure:

- 50% LTV Conventional 1st DOT/Mortgage

- 40% LTV SBA/CDC 2nd DOT/Mortgage

- 10% Equity Injection

SBA 504 Program Eligibility:

- The Small Business Concern must be operated for profit and fall within the size standards set by the SBA (Tangible Net Worth LESS THAN $15 million and Average Net Income DOES NOT exceed $5 million after taxes for the preceding two years). Loans cannot be made to businesses engaged in speculation or investment in rental real estate.

Use of Proceeds:

- Purchasing land and improvements, including existing buildings, grading, street improvements, utilities, parking lots and landscaping.

- Construction of new facilities or modernizing, renovating or converting existing facilities.

- Purchasing long-term machinery and equipment.

NOTE: The 504 Program cannot be used for working capital or inventory, consolidating or repaying debt, or refinancing.

Maximum Debenture:

- $1,500,000 when meeting the job creation criteria or a community development goal.

- $5,000,000 when meeting a public policy goal.

- $5,500,000 for small manufacturers.

Debenture Rates/Fees:

- Interest rates on 504 loans are pegged to an increment above the current market rate for five-year and 10-year U.S. Treasury issues. Maturities of 20 and 25 years are available. Fees total approximately 3 percent of the debenture and may be financed with the loan.

Eligible Property Types:

- Office: Professional, Condominimum, Medical, Dental and Veterinarian.

- Industrial: Heavy and Light Manufacturing, Warehouse and R&D Flex.

- Retail: General.

- Special Purpose: Assisted Living Facilities / Adult Care, Day Care Facilties, Restaurants, Funeral Homes and Hotels/Motels.

Maximum Loan Amount:

- 1st DOT/Mortgage – $12,000,000

Rate Options:

- 3, 5, 10, and 25-Year Fixed Loan Terms Available.

Maturity and Amortization:

- Up to 25 and 30 years.

Maximum LTV:

- 60% LTV based upon the Lower of Cost or Apprasied Value.

Minimum Debt Coverage Ratio:

- 1.10x Minimum Debt Coverage Ratio (“DCR”) for the most recent FYE and Interim period. The DCR will be based on the underwritten EBITDA of the Small Business Concern.

Occupancy:

- 51% or greater must be occupied by the Small Business Concern.

Borrower/Guarantor Characteristics:

- Prior Ownership and Management Experience.

- Minimum FICO 680.

Recourse:

- All loans are Full Recourse and require the personal guarantee of any and all individuals or entities holding 20% ownership interest or more.

Interim Financing:

- Up to $5,500,000

- 120 Day Term.

- Variable Interest Rate based upon the published Wall Street Journal (WSJ) Prime Index + 2.75%, Interest Only, to adjust QUARTERLY.

**Funding of interim loan may be required by Lender.

Construction Financing:

- Available for Multi Purpose Projects. Please call for Program Information.

CONTACT

HORIZON SMALL BUSINESS LENDING SOLUTIONS

110 West Center Street

Bountiful, UT 84010

Keldon R. Moldre

Jason M. Charles

Loan Intake Form

Buying vs. Leasing Checklist

Top questions to ask if you’re considering

purchasing commercial property

Review your business’ needs for today and tomorrow

-

MY TIMELINE

How long do I intend on occupying a commercial property with my business?

-

APPEARANCE + LOCATION

Do I need my building to look a certain way, or be in a certain location?

-

CURRENT LEASE

How much time is left on my lease, and if longer than 12 months, am I happy to renew again or where am I going once that lease is up?

-

WHO’S IN CONTROL

Am I comfortable knowing that when renting, my landlord can choose not to renew my lease, may not maintain the property to my liking and can increase my rent? Would any of these actions jeopardize my business?

-

VISION

What is the long-term vision for my business growth; do I need a larger space and/or a specifi c confi guration to support my goals?

Review your business’ needs for today and tomorrow

-

AFFORDABILITY

Do I have enough liquidity in my personal and business accounts for the down payment and additional closing costs without impacting my business operations?

-

DOWN PAYMENT

Will an SBA 504 commercial real estate loan that only requires a 10% down payment or a conventional loan that requires a 20% owner injection make more sense for my business fi nancially?

-

PREDICTABLE – FIXED COST

Would my business benefi t from a predictable fixed cost for my building occupancy expense?

-

RENTAL RATES

Have rising rental rates affected my earnings?

-

BUSINESS STRUCTURE

Is there more than one owner of the business? If so, what is the percentage ownership and who will be required to guarantee a loan?

-

MONTHLY PAYMENTS

Will buying yield me cost savings on a monthly basis and what does that estimate look like?

-

TAX BENEFITS

Will I see any tax benefi ts if I own a building? A consultation with a trusted fi nancial planner or CPA can help you answer this question.

-

RETIREMENT

Do I see adding real estate to my personal fi nancial portfolio as a component of my retirement plan?

Evaluate the idea of being your own landlord

-

OWNERSHIP

Can I handle the responsibility of owning and maintaining a commercial property?

-

WHY BUY?

Will buying a commercial building support my business goals or my personal fi nancial portfolio or both? Are my reasons smart and strategic?

TOP 3 REASONS SMALL BUSINESSES SHOULD BUY A BUILDING INSTEAD OF LEASING

Small business owners who are tired of paying rent for their business or commercial building or have an upcoming lease renewal, should know there’s an alternative to renting – buying your own building through an SBA 504 real estate loan.

“Instead of writing a check to a landlord every month, business owners can be paying themselves – investing in their future,” said Kurt Chilcott, president of CDC Small Business Finance, the nation’s leader in SBA commercial real estate lending and 504 loans.

SBA 504 loans are provided in partnership between certified development companies, or CDCs, and banks. SBBA 504 loans provide small business owners below-market, fixed interest rates.

WHAT ARE THE BENEFITS OF AN SBA 504 LOAN?

There are many reasons to own your building instead of renting. The Top three reasons to own a commercial building are:

- Build equity – every payment made is an investment in a business owner’s future. They can leverage the accumulated wealth for future business growth or new options when the time comes to retire.

- Stabilize occupancy costs – you don’t have to worry about unexpected rent increases – the monthly payment is always the same. SBA 504 loans offer a fixed rate for 25, 20 or 10 years.

- Preserve cash – in many cases, the monthly payment to own is less than the rent. Small business owners can use that working capital for other things that can help grow their business, like to buy inventory, hire new employees, equipment financing or invest in other strategies to grow or improve the business.

Case in point: A California-based manufacturer used a $2.4 million SBA 504 loan to buy a building. His company expects to save $2,000 a month by owning the building versus renting it.

Another benefit of SBA 504 loans is tax savings. Just like a home mortgage, interest on commercial real estate loans are tax deductible.

25-YEAR SBA 504 LOANS ARE NOW AVAILABLE

The Small Business Administration (SBA) recently started taking applications for the new 25-year term SBA 504 loan, designed to complement the 20-year and 10-year terms traditionally offered with 504 loans.

The purpose behind lengthening the payment cycle on a 504 loan is to cut monthly loan payments for borrowers, considering rising operating expenses and interest rates.

WHAT IS THE ‘GREEN’ PROVISION?

Small business entrepreneurs are discovering other advantages of SBA 504 financing, including the “green” provision, which allows higher lending amounts for small business owners who want to buy or improve commercial or industrial buildings to make them more energy efficient.

To qualify for the Green Provision, smallbusiness owners need to demonstrate a projected 10 percent reduction in energy costs by implementing one or more energy-saving improvements (e.g. insulation, energy-efficient lighting, more efficient heating/air conditioning, etc.).

![]()

Loan Calculator

Calculate your estimated monthly and annual loan payments for a small business loan (504 loan).

This tool was designed only to provide an estimate for SBA 504 loans. Loan terms and rates may vary.

Please correct the following error(s).

| Source | Amount | Rate | Term | Monthly Payment | Annual Payment |

|---|---|---|---|---|---|

| Bank Loan | $0 | 0.00% | 0 | $0 | $0 |

| SBA 504 Loan | $0 | 0.00% | 0 | $0 | $0 |

| Down Payment | $0 | ||||

| Totals | $0 | $0 | $0 |